Many of you reading this article will know of recent business failures, some of which will have had a direct impact on your own business. Sadly, many of these failed businesses may well have been profitable and failed simply because they ran out of cash. The importance of cash to a business can easily be compared to the importance of air to a human – cut off the supply and the end is imminent.

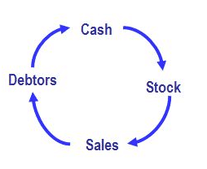

In a typical business the cash cycle looks something like this:

In the above model you start your business by using cash to purchase stock. You then sell some stock (hopefully for more than it cost!), converting your stock into debtors. Once you are paid by your debtors the cash returns to you and the cycle begins again. Obviously in some businesses (for example a service business), stock in the above model can be replaced with work-in-progress and in others there may be no debtors as all sales may be paid for in cash. However, regardless of the business, a variation of this model will apply.

The more you can accelerate the cash cycle outlined above, the faster you turn your profits into cash and the easier it is to manage your working capital position. Aside from the obvious issues, such as generating sufficient sales and having suitable margins, the areas that typically cause cash flow problems are the following:

- Carrying Too Much Stock – ideally a business should carry no more stock than it needs in order to maximise sales. Slow moving or obsolete stock needs to be liquidated and turned back into cash. Monitor stock turn rates, create sound relationships with suppliers to shorten lead times and know your market so that you don’t end up with hard to move items. It is also worth noting that there is a proven link between high stock levels and an increase in both stock theft and damage.

- Inadequate Debtors Control – take a look at the way you manage debtors and here the payment process can be tightened up. Monitor your debtors’ days and implement a robust collection system. Late payers need to be brought under control now to minimise the impact on your cash flow. In this market customers will take every opportunity to delay payment and those businesses without tight credit controls are invariably the last to be paid. Don’t forget that it’s costing you money every day to fund your overdue debtors, so charging interest is a valid option.

- Capital Expenditure – be wary of paying cash for any significant capital items unless you have robust cash flow forecasts in place that show the purchase can safely be done. Many businesses run into trouble because they used their cash to fund asset purchases and then later couldn’t pay their tax bills or their suppliers. Remember, you can finance or lease your equipment purchases so that you are not putting pressure on your cash flow. A good rule is to match the life of the loan with the life of the asset.

- Drawings – as a business owner, how much money are you taking out of the business on a monthly basis? Many business owners are shocked to see the annual level of drawings that they take and are unaware of the pressure that this can put a business under. Set yourself a budget that is acceptable to both you and your business and stick to it.

One of the simplest and most valuable business tools you can have is some solid cash flow projections. For some businesses they find that they can operate on projections that show a month end cash position only while others need weekly or even daily cash projections to keep things on track. Projections let you see potential cash flow problems in advance and deal with them before you reach a crisis point.

There are many aspects to the business cash cycle that can be managed. EPPL currently has the specialist systems and the expertise to help you manage your cashflow to your specific goals. Contact us to find out how info@eppl.co.nz or call us 09-636-3332.